Navigating the Application Process for Small Business Loans

Start with Solid Preparation

- Before approaching any lender, clearly define why you need the loan and how you'll use the funds. Lenders want specific details, not vague requests for "working capital." Whether you're purchasing equipment, expanding inventory, or hiring employees, have concrete numbers and explanations ready.

- Assess your business's financial health honestly. Review your cash flow, profit margins, and existing debt obligations. Understanding these metrics helps you choose the right loan amount and identify potential concerns before lenders discover them.

Gather Essential Documentation

The documentation phase often determines application success. Start collecting these materials early:

- Personal Documents: Tax returns from the past two to three years, personal financial statements, and bank statements. Since many small business loans require personal guarantees, your personal financial history matters significantly.

- Business Documents: Profit and loss accounts, balance sheets, company tax returns, and cash flow statements. If you're a newer business, include detailed financial projections showing how you'll repay the loan.

- Legal and Operational Papers: Business licenses, articles of incorporation, lease agreements, and any contracts that demonstrate your business's legitimacy and operational foundation.

Choose Your Application Path

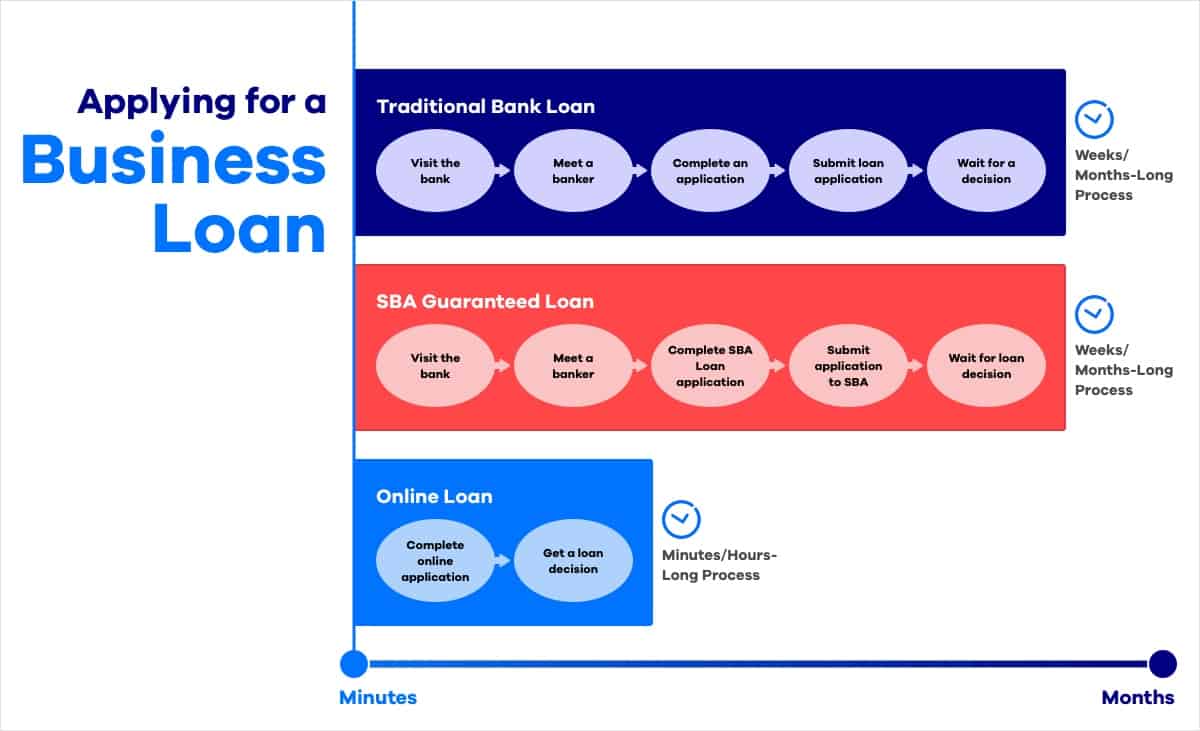

- Different lenders offer varying experiences and requirements. Traditional banks provide relationship-based service with competitive rates but typically have stricter requirements and longer processing times. Online lenders offer speed and convenience, often providing decisions within days, though interest rates may be higher.

- SBA loans require more documentation and time but offer excellent terms for qualifying businesses. Alternative lenders may accept lower credit scores but charge premium rates.

Navigate the Application Process

- Most applications follow predictable stages. Initial submission involves completing forms and providing basic documentation. Lenders conduct preliminary reviews to ensure you meet minimum requirements before moving to detailed underwriting.

- During underwriting, lenders analyze your business thoroughly. They may request additional documentation or clarification. Respond promptly and completely to keep your application moving forward. Depending on the lender and the intricacy of the loan, this phase might last anywhere from a few days to several weeks.

Avoid Common Mistakes

- Incomplete or inconsistent documentation kills more applications than any other factor. Ensure all information matches across documents and that nothing is missing or outdated.

- Don't request unrealistic loan amounts. Conservative requests backed by solid justification perform better than aggressive proposals that exceed your clear repayment ability.

- Timing matters too. Avoid applying during your business's slow seasons or when experiencing temporary financial difficulties.

Work Effectively with Lenders

- Treat loan officers and underwriters as partners, not adversaries. Be responsive when they request information and honest about any challenges your business faces. Transparency builds trust and credibility.

- If lenders visit your business location, ensure it's organized and professional. These visits help them verify that your operation matches your application description.

Prepare for Approval Conditions

Most approvals come with conditions that must be met before funding occurs. Common requirements include updated financial statements, specific insurance coverage, or additional documentation. Having systems in place to meet these conditions quickly accelerates the final funding steps.

Learn from the Experience

Whether successful or not, every application teaches valuable lessons about your business's financial position and how lenders evaluate risk. Use these insights to strengthen future applications and improve your overall financial management.

Bottom Line

The small business loan application process requires preparation, patience, and persistence. By understanding what lenders need, preparing thoroughly, and maintaining professional communication throughout the process, you significantly improve your approval odds. Remember that lenders want to make good loans to qualified businesses – your job is to demonstrate clearly that you represent a sound investment opportunity.