Are MCAs Legal in All 50 States?

Why MCAs Are Legal Everywhere

- They're sales, not loans: MCAs are designed as purchases of future credit card receivables, rather than standard loans.This legal distinction allows them to operate outside many banking regulations and interest rate caps that apply to conventional lending.

- Commercial transactions have fewer restrictions: Since MCAs are business-to-business transactions rather than consumer loans, they're exempt from many consumer protection laws that govern personal credit.

- Interstate commerce protections apply: Most MCA providers operate across state lines, which gives them certain federal protections that can override some state-level restrictions.

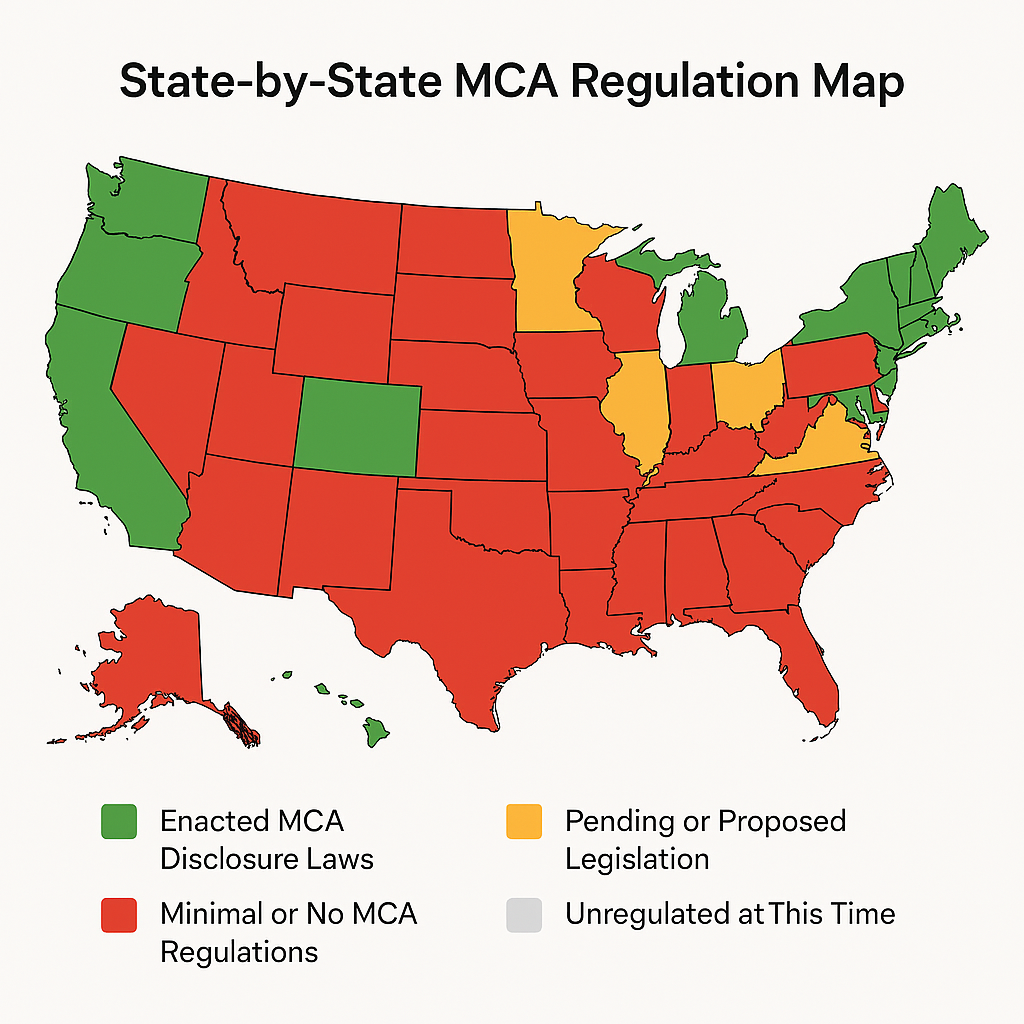

Three Types of State Regulation

- Heavy regulation states like New York and California require detailed cost disclosures, standardized contract language, and clear APR calculations. These states offer the most protection for businesses but may have fewer provider options.

- Moderate regulation states such as Florida require basic licensing and operational standards but don't mandate extensive disclosures. You get some protection without overly restrictive rules.

- Minimal regulation states including Texas and many others rely primarily on general business law and fraud protections. This creates more provider options but requires extra caution from business owners.

What Protection You Have Everywhere

- Basic contract law applies: All MCA agreements must follow fundamental contract principles. Providers can't use fraudulent, misleading, or unconscionable terms regardless of state-specific MCA laws.

- Fraud protection exists in every state: If a provider misrepresents terms, hides fees, or uses deceptive practices, general business fraud laws provide legal recourse.

- Collection practices are regulated: Debt collection laws limit how aggressively MCA providers can collect payments, even though specific MCA collection rules vary by state.

Red Flags That Are Problematic Anywhere

- Unlicensed operators: Even in minimally regulated states, MCA providers typically need basic business licenses. Always verify proper licensing.

- Confession of judgment clauses: These allow providers to seize assets without normal legal processes. Several states have banned them, and they're risky everywhere.

- Extreme costs or deceptive practices: While rate caps may not apply, extremely high costs or misrepresentation can violate general unfair business practice laws.

How to Protect Yourself

- Research your state's specific laws: Contact your attorney general's office or state banking department to understand what protections exist in your location.

- Verify provider credentials: Ensure any MCA provider is properly licensed in your state and check for regulatory complaints or actions.

- Demand full transparency: Regardless of state requirements, insist on complete information about costs, terms, and collection practices before signing.

- Read contracts carefully: Understand all terms, fees, and obligations. Don't rely on verbal promises—everything important should be in writing.

Current Trends

- More states are adding oversight: The trend is toward increased regulation, with more states implementing disclosure requirements and operational standards each year.

- Focus on transparency, not bans: Most new regulations emphasize helping businesses understand costs and compare options rather than prohibiting MCAs entirely.

- Federal attention is growing: While there's no federal MCA regulation yet, agencies are monitoring the industry and may eventually implement national standards.

The Bottom Line

MCAs are legal nationwide because of how they're structured, but your level of protection depends heavily on where your business is located. States with strong oversight provide better safeguards, while those with minimal regulation require more vigilance from business owners.

Regardless of your state's legislative framework, success with MCAs demands working with trusted suppliers, understanding all terms and fees, and ensuring the financing meets your company's objectives. Stay informed about your local laws and don't hesitate to seek professional advice for significant financing decisions.